Caravel Minerals has increased the likelihood that sufficient tonnages may now exist at its namesake copper play in the Wheatbelt to support a higher grade start-up project after receiving further assay results from its recently completed diamond drilling program.

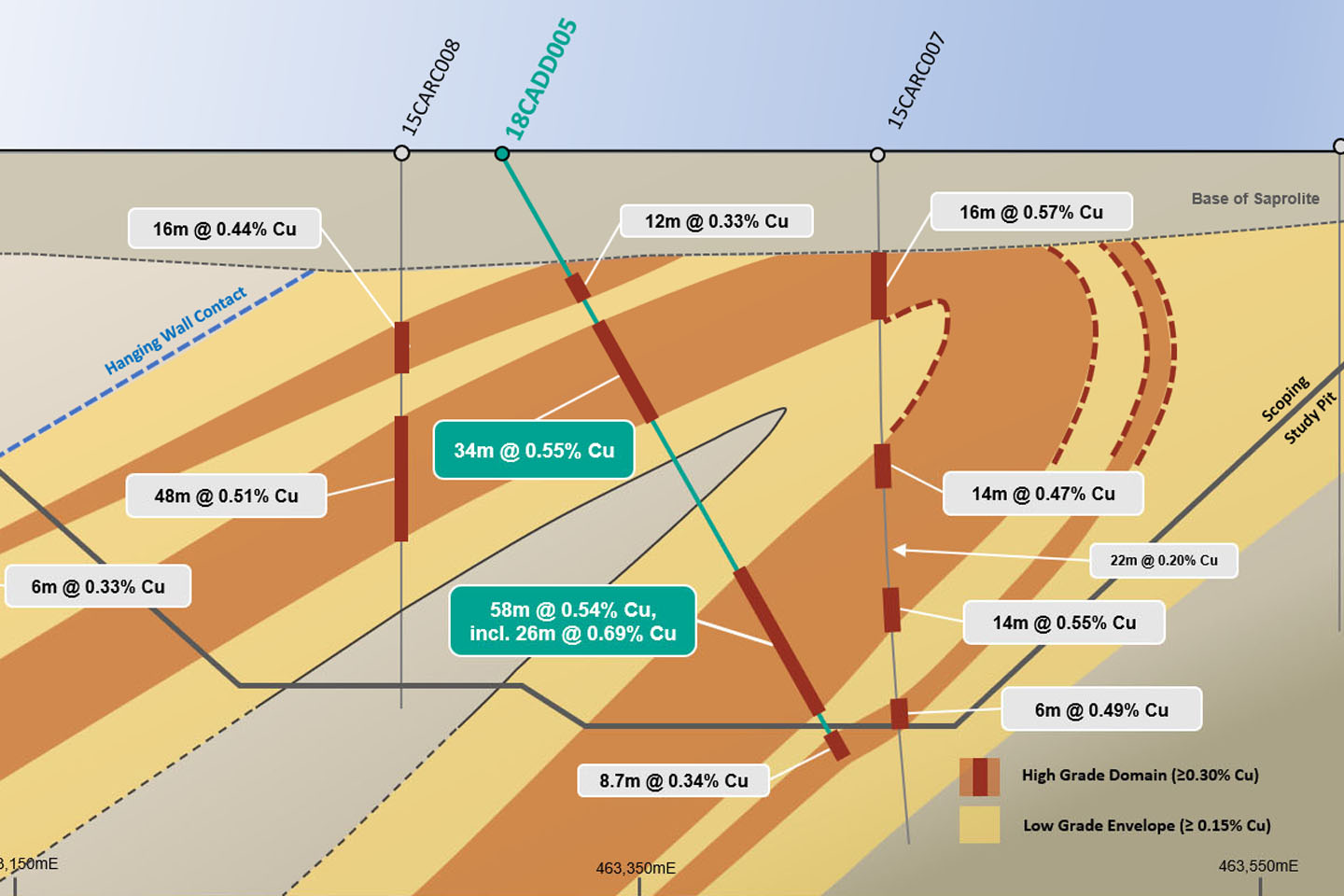

The new results confirmed the presence of thick, higher grade zones at the Bindi Hinge zone of 34m grading 0.55% copper from 64m down-hole and 58m @ 0.54% copper from 150m including 26m @ 0.69% copper from 182m in the same hole.

Mineralisation in both zones remains open at depth.

Importantly, both the mineralised zones and grades are higher than previously modelled.

Management said the results have confirmed the multi-domain geology model for Bindi Hinge over more than 1.6km of strike.

According to the company there is now significant potential for notable improvements to the current resource model with Caravel planning further work to examine downdip extensions of the east limb that remain untested by drilling.

The latest results back up assays from earlier holes in the program that were reported back in November last year, which included results of up to 6m @ 1.03% copper incorporated within a broader zone of 20m @ 0.5% copper from 94m deep.

Another hole, completed 400m to the north turned up a 30 metre mineralised zone assaying 0.55% copper from 100m down-hole that contained a higher-grade intercept of 18m @ 0.8% copper from 102m deep.

Caravel expects to complete a new resource estimate that incorporates the latest results early this year.

This will provide the basis for revised pit designs and mine schedules that could support an alternative development model based on initial mining of the higher grade zones.

The Caravel project currently has a mineral resource estimate of 402 million tonnes @ 0.29% copper, which comprises the flagship Bindi West and Bindi East deposits and the satellite ore systems at Dasher and Opie, located further to the south.

Despite its relatively modest grade, the project has a remarkably low stripping ratio of just 1:1 and low cash operating costs compared to its peer group of companies with similar size and grade copper deposits globally.

A previous scoping study showed an operating cash flow figure before tax of USD$2b over its extraordinarily long initial mine life of 21 years with capital paid back in just 3 years.

The new results represent a solid start to the new year for Caravel and with the potential to start mining in higher grade zones now, the previous, already impressive scoping study financials will no doubt need to be updated.